- The Spring Statement proved to be relatively low-key with the main policy change being the pre-announced adjustments to welfare spending. Through this, the UK government has restored its fiscal headroom to exactly where it was in October after the buffers were subsequently been eroded by higher interest costs and slower growth.

- While proof of commitment to the fiscal rules is always welcome, the narrow headroom again leaves the government hostage to fortune in a volatile global environment. The OBR forecasts on growth and productivity look typically optimistic. We continue to expect tax rises will be required at the full Budget in the autumn in order to put UK public finances on a more sustainable footing.

- The financial market impact therefore has been modest and we do not see any risk of delayed impact. Gilt yields are lower with no unfavourable Gilt supply implications while lower rates, in part due to weaker than expected CPI this morning has resulted in a modest GBP drop.

Macro view: Sailing close to the wind

The UK’s fiscal buffers have been restored, just

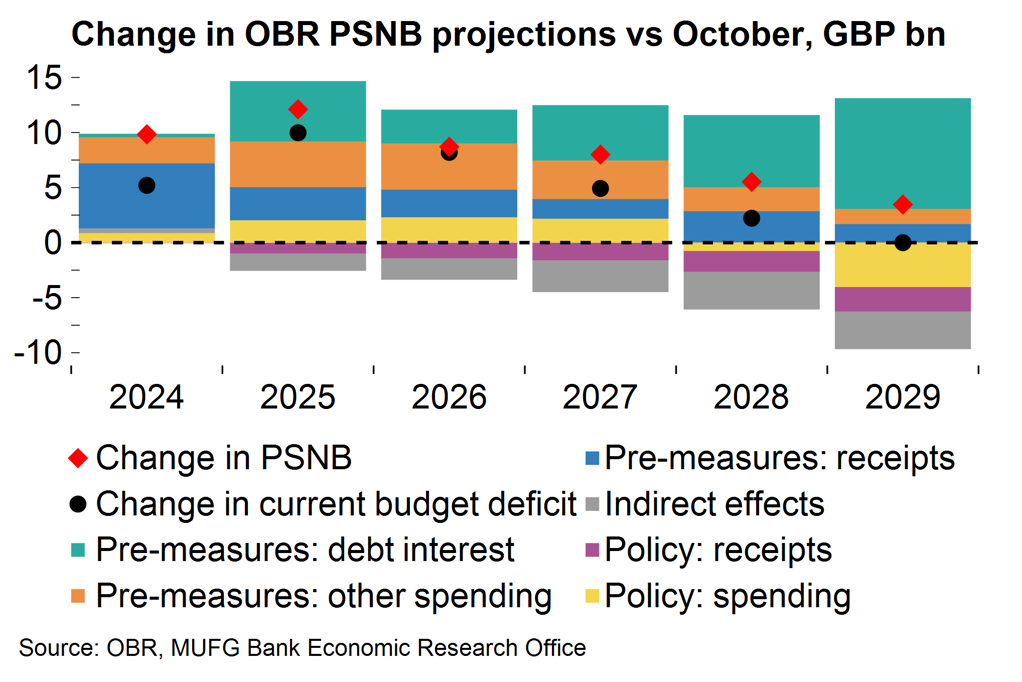

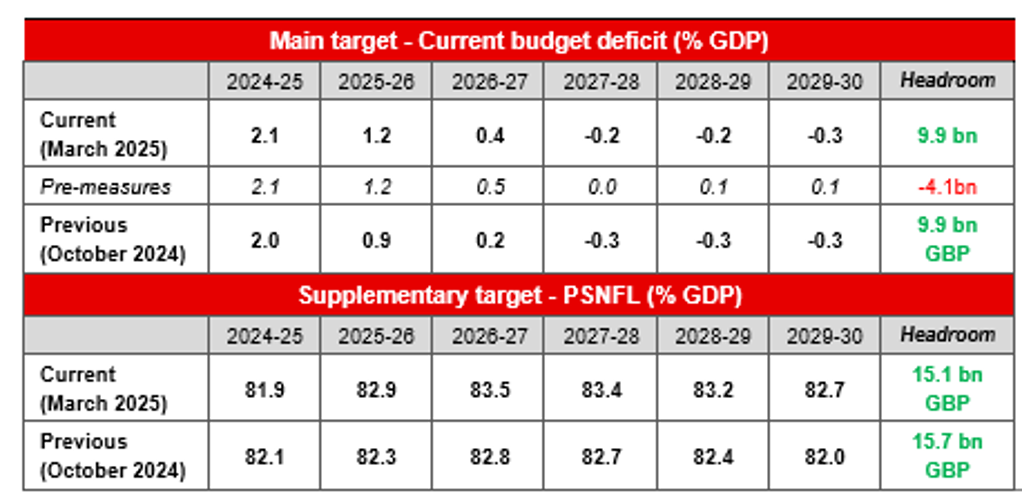

As expected, the OBR’s updated forecasts confirmed that the government’s headroom against its fiscal rules had been wiped out by a combination of higher debt interest spending and weaker receipts. The pre-measures forecast put the current budget deficit, which is required to be balanced, at 0.1% of GDP at the end of the projection horizon (a 4.1bn overshoot).

Higher interest costs and lower receipts eroded the fiscal headroom

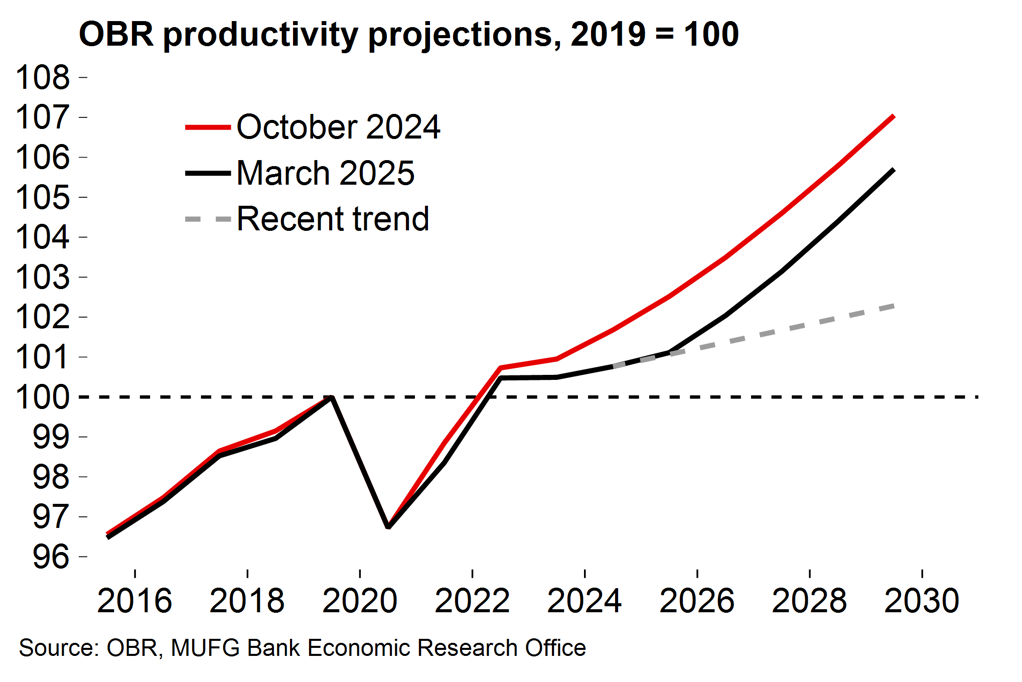

The OBR’s productivity forecasts may well prove to be optimistic

Pre-announced welfare spending reform, shifting of overseas aid to defence (where associated capex is not included in the fiscal target), and a favourable interpretation of the economic impact of the government’s planning reforms restored this headroom to exactly the same mark as before: 9.9bn, or 0.3% of GDP, by 2029-30.All told, there were no fireworks with the government doing its best to stick to its commitment for one ‘major’ fiscal event a year.

The upshot is that the can is probably being kicked down the road on the more difficult decisions. If the headroom against the fiscal rules looked slim back in October it looks wafer-thin now given heightened global uncertainty. The government may well come to rue not giving itself more of a buffer.

The government may rue not giving itself more headroom

There are several sources of risk. The OBR’s growth forecasts look typically optimistic. The projection for 2025 was downgraded from 2.0% to 1.0% (which is in line with our latest) and their current estimate of 1.9% in 2026 may also be hard to reach (MUFG: 1.5%).

Further ahead there is still the looming threat that the OBR will be forced to materially downgrade its productivity assumptions. The OBR highlighted that the current budget would be in deficit by 1.4% of GDP in 2029-30 if productivity continues along its current trend of just 0.3% annual growth rather than returning to a trend of 1.3%, so the stakes are extremely high.

OBR fiscal rules projections

Source: OBR March 2025 projections.

We continue to expect the government will be forced to hike taxes, eventually

Even in the absence of more meaningful defence pledges, our view remains that the government will be forced to increase taxes at some point during this parliament to restore UK public finances to a stable footing. Moving the goalposts by tinkering with the fiscal rules again would clearly be damaging for credibility and likely result in counterproductively higher borrowing costs.

If tax rises are indeed implemented, the government might opt to go along the well-trodden ‘stealth’ route by leaving income tax thresholds frozen (rather than uprated with inflation) beyond 2028, which is the current plan. The hope would be that growth conditions improve which frees up headroom and allows for some pre-election tax cuts.

Any tax rises would be a huge challenge in terms of official communication. The government bungled the messaging around its first budget by announcing months in advance that there would be ‘painful’ measures, without providing any guidance about where the axe might fall. Unsurprisingly, that encouraged speculation which weighed heavily on sentiment indicators and contributed to the UK economy losing momentum sharply in H2 2024.

Let’s hope that lessons have been learned but, in short, there are no easy options for the government. The UK simply does not have the fiscal space to implement the sort of blockbuster fiscal stimulus announced in Germany (see here). Indeed, our suspicion remains that the need for trade-offs will only increase further on the back of greater defence requirements.

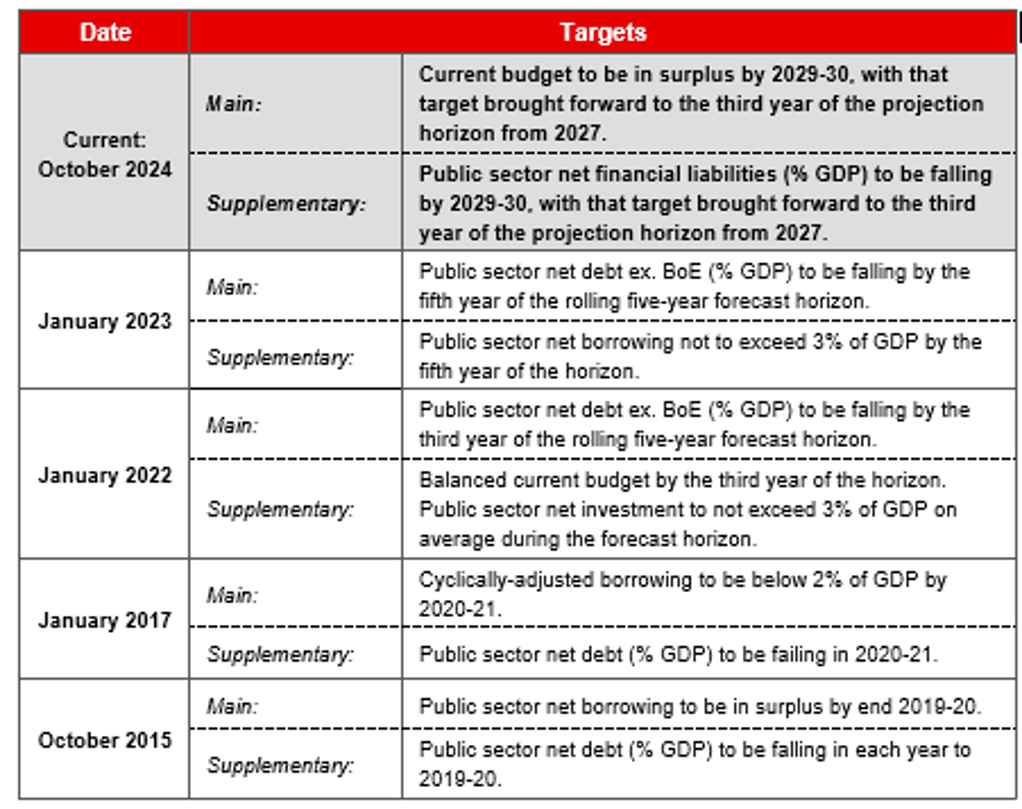

UK fiscal rules since 2015

Source: OBR and related legislation

Markets view: Limited implications with credibility restored for now

Since the Gilt sell-off in January that brought home the need for action to restore fiscal credibility, the pound (BoE TWI basis) has advanced close to 3.5% from the low in the middle of January. As implied above, many aspects of the today’s budget statement were already in the public domain and hence there were no major surprises. The pound is therefore only marginally weaker and the bulk of the decline reflects the weaker than expected CPI print this morning that increases the prospect of a 25bp rate cut by the BoE on 8th May.

The government have managed to achieve its objective for today – to restore a level of credibility to the fiscal outlook – and will help alleviate the risk of a repetition of what happened in January – a Gilt sell-off that coincided with a pound sell-off. At least over the near-term, a reduction in fiscal risks should help encourage increased appetite for holding the pound. Positioning flows have already been in that direction with both Leveraged Funds & Institutional Investors buying the pound since the start of February.

While near-term fiscal risks have eased, incoming weak economic data and broader financial market volatility could undermine fiscal confidence and see risks re-emerge at a later date given the fiscal headroom is relatively small. The big event risk now is “Liberation Day” and the announcement of the reciprocal tariff plans by President Trump. The pound could benefit if as expected the UK avoids aggressive action.