- The UK Labour party remains comfortably on course win next week’s general election after 14 years in opposition. Labour’s manifesto is unassuming – there is clearly no desire to rock the boat on the fiscal front – but there are some growth-friendly policies in there, most notably on planning reform. However, the most significant shift is that a new government with a sizeable majority would represent a return to relative calm and stability after the turbulence of the Brexit years and five prime ministers in eight years. That is likely to support investment and activity more broadly.

- Overall, we are cautiously optimistic about the medium-term UK outlook and our base scenario is growth of 1.6% in 2025. That would be a welcome acceleration after what has been an extended period of stagnation prior to this year.

To read the full report, please download the PDF above.

Labour still on course to form the next government

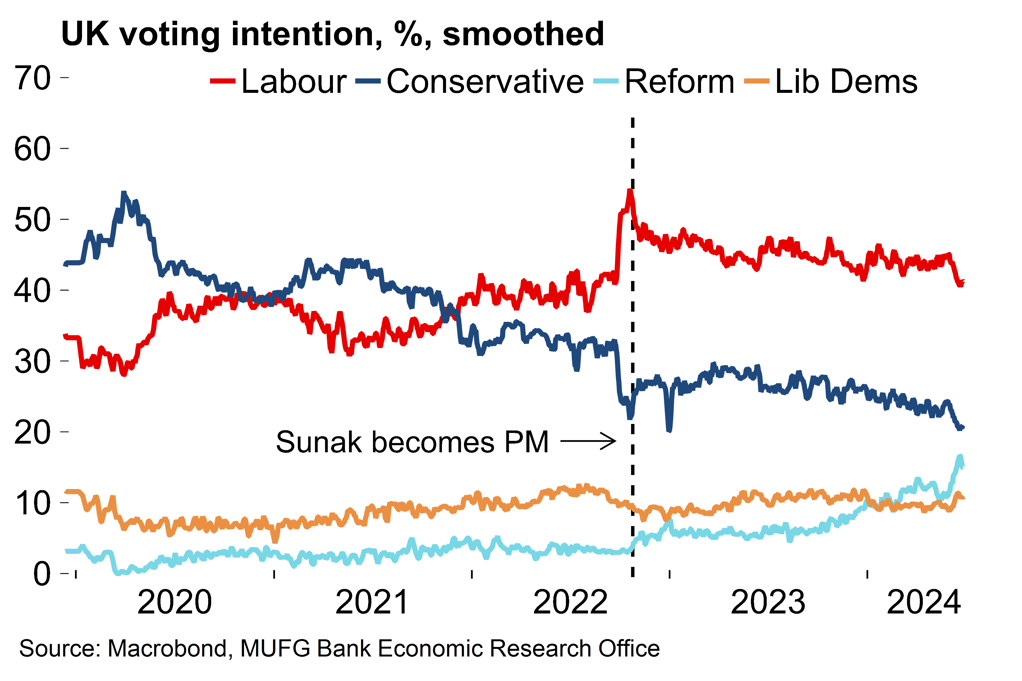

The Labour party remains on course to win the UK general election on 4 July, and win it comfortably. When Sunak, the UK PM, took the surprise decision to call the vote last month we suggested that his Conservative party’s polling deficit could narrow slightly (see here). That has not been the case. The Conservatives have suffered from numerous campaign missteps and the rise in support for the right-wing populist Reform UK party since Nigel Farage, the architect of Brexit, entered the contest as a candidate. Labour have consistently led the polls since late 2021 and by-election and local election results have provided no reason to question the accuracy of this. Prediction markets now put the implied probability of a Labour majority at over 95%.

Chart 1: Labour’s lead has remained stable since Sunak became prime minister

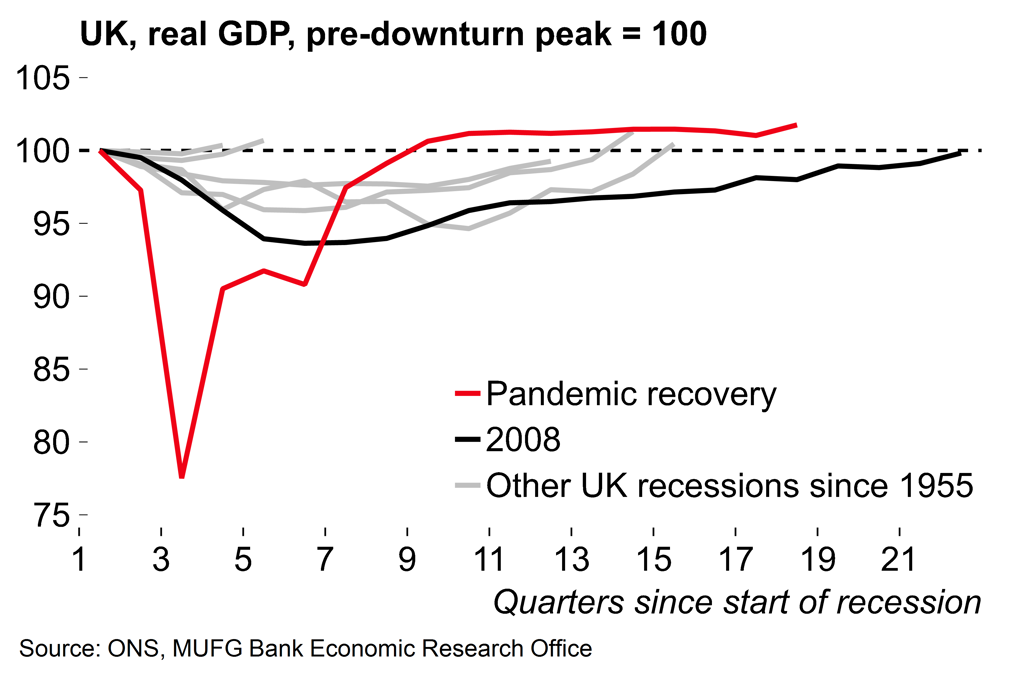

Chart 2: The UK economy has experienced an extended period of stagnation since the post-pandemic rebound

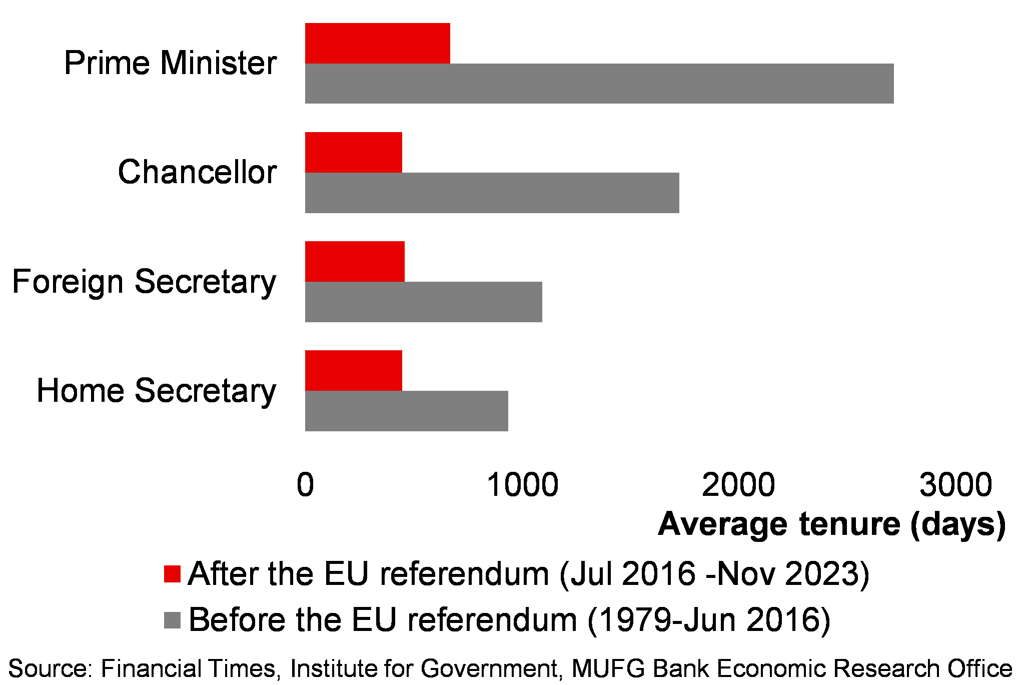

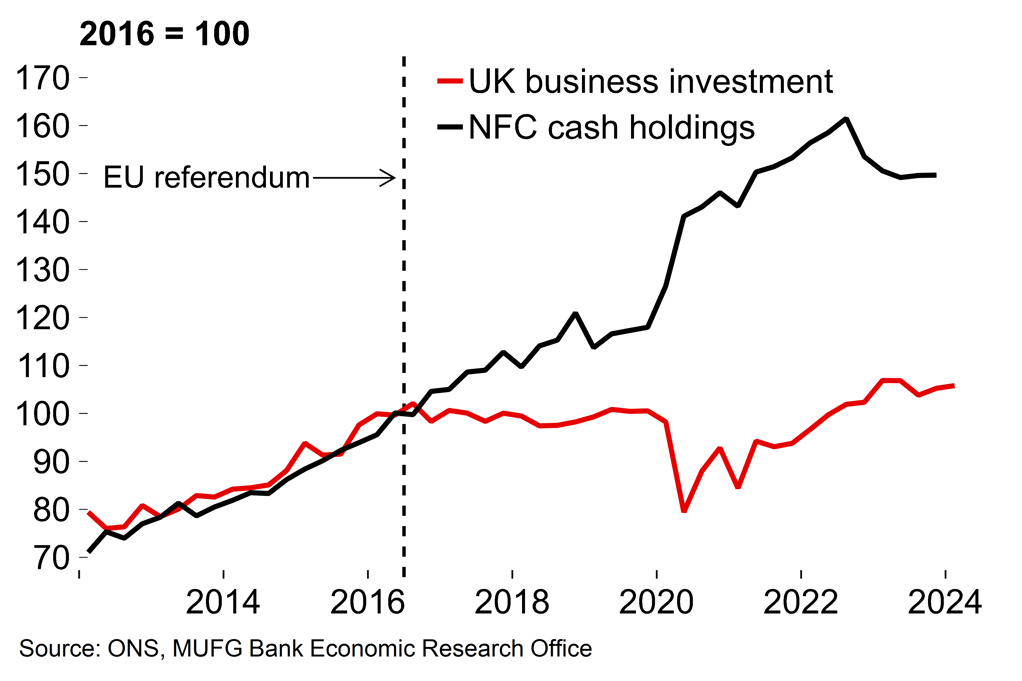

The Labour Party in its current incarnation is moderate and centrist. It has strongly indicated that it would follow a pro-business approach while erring on the side of caution when it comes to public finances. The manifesto (full document here, summary in the PDF version of this note) reflects this stance with a coherent but unassuming set of policies. Essentially the pitch is that sound management and political stability will create better growth conditions. We believe there’s some truth in that, all else equal. The UK has had five prime ministers in eight years and high leadership churn in the majority of government departments which has resulted in frequent policy shifts. As well as the uncertainty around what shape the Brexit deal would take, the opportunity cost of leaving the EU has also been high with policymakers focusing on little else for an extended period. Against that background, UK business investment has increased by just 3.6% since Q3 2016, which leaves clear scope for an extended recovery.

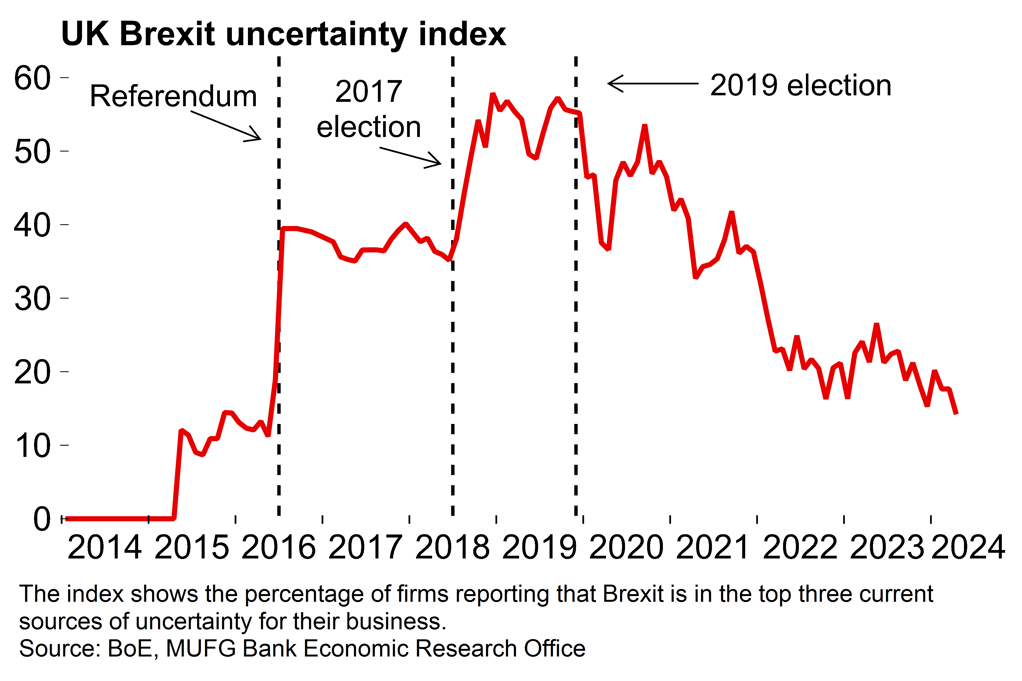

On Brexit, we don’t expect a significant change in EU-UK trading relationship. Labour will want to be seen to be at least trying to make Brexit work and there is little appetite on the EU side to re-open meaningful negotiations. That said, the party has indicated that it will seek to decrease some of the current frictions by looking to limit some border checks and expand the mutual recognition of qualifications for service-sector workers.

Chart 3: The turnover of cabinet ministers increased significantly since the EU referendum

Chart 4: Some firms still cite Brexit as a source of uncertainty

Labour’s cautious programme does not point to radical change

The most significant policy proposal from Labour is the aim to shake up planning restrictions to make it easier to build in the UK. The target is to build 300,000 new homes each year. That would certainly be positive for growth and the commitment seems genuine. While the UK does have plenty of developable land, it may be hard to achieve. Successive governments have had similar aims yet fallen well short in the face of deep-rooted and effective nimbyism in the UK – an average of just 180,000 new homes have been built annually since 2000. It’s also worth noting that there are 500,000 fewer people employed in the construction sector compared to the pre-pandemic peak of 2.6m, so any meaningful increase in output is unlikely to happen quickly.

Other proposals include some Bidenomics-inspired (but much more modest) active industrial policy, with a focus on trade, manufacturing and clean energy. The new ‘National Wealth Fund’ would invest 7.3bn GBP of public money over the course of the next parliament, with the aim of attracting three times that in private investment (which seems plausible). Again, it looks good on paper but the sums are modest and in isolation it is unlikely to move the needle in terms of growth or productivity.

Indeed, a common criticism of Labour’s policy proposals has been that they are too cautious and will do little to address some of the UK’s long-term structural issues. Labour has ruled out any increases in income tax, national insurance, VAT or corporation tax (which are the main sources of government revenue) and pledged trivial amounts of new day-to-day spending, in areas such as health, education and policing (see Table 1).

With the Liz Truss debacle still fresh in memories it’s clear that there is no desire to rock the boat when it comes to fiscal policy. The shadow chancellor, Rachel Reeves, is a former BoE economist and seems instinctively cautious. Labour will tweak the current fiscal rule which limits the deficit to 3% of GDP in the fifth year of the forecast by moving to a balanced day-to-day budget, but allowing borrowing for investment.

That is a sensible shift (UK investment-to-GDP has long trailed behind most peers), but still won’t afford much room for manoeuvre. Labour will retain the current, primary fiscal rule that debt-to-GDP should be falling over the medium-term, with no distinction made for whether that debt was accrued through borrowing for current or capital expenditure. While the rolling horizon makes it easy to game this rule by backloading any politically painful decisions, the headroom against the target is wafer-thin and only modest investment spending is credible on current projections. Labour’s manifesto claims there will be GBP 3.5bn of extra annual borrowing for investment – just 0.1% of GDP.

That said, we suspect that the current government’s recent national insurance tax cuts, which can essentially be seen as pre-election giveaways, may well be at least partially reversed under Labour (despite the manifesto pledge to leave the rates unchanged). There could be some political leeway to do so early on (e.g. “we can now look at the books in more detail and unfortunately the previous government has left public finances on an unsustainable path”) but it would certainly shorten the ‘honeymoon period’ for the incoming government. At any rate, the tax burden is set to continue to increase with Labour maintaining the Conservatives’ policy of leaving tax thresholds unchanged rather than increasing them in line with inflation. This fiscal drag is set to see the UK’s tax-to-GDP ratio rise from 33.5% in 2021 to above 37% by 2028 based on OBR forecasts.

These forecasts are dynamic and a clear point of difference between a Labour and Conservative government is how any increase in fiscal headroom – e.g. from faster-than-expected growth or lower interest rates – would be used. In that case, the Conservatives would continue to prioritise tax cuts while Labour would increase spending, whether on public services or capital investment.

Chart 5: There is clear scope for an investment bounce in a more stable business environment

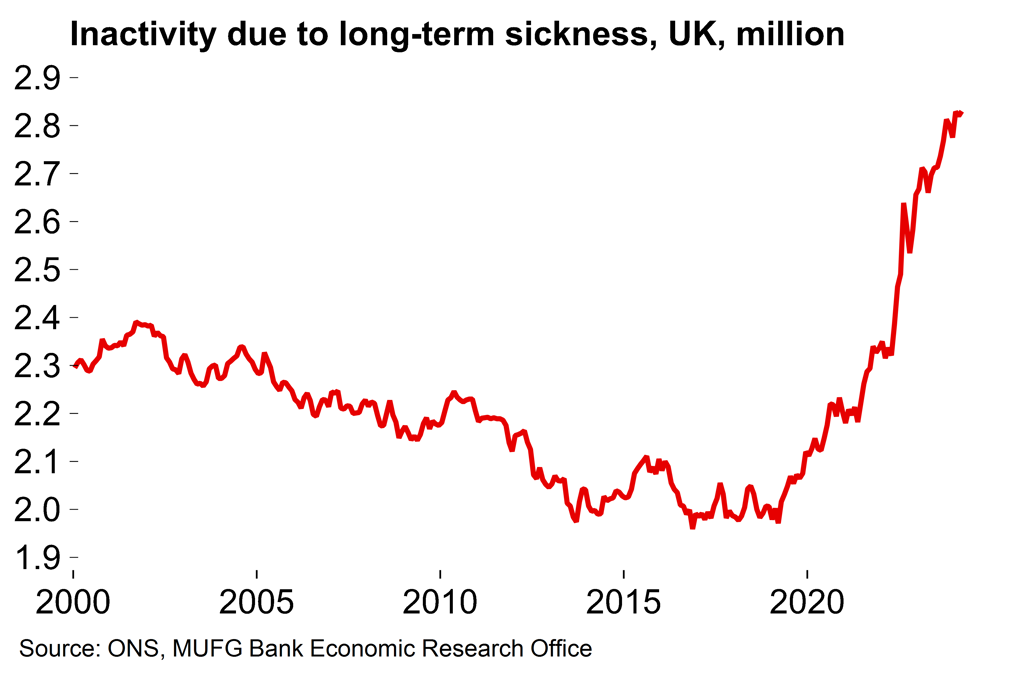

Chart 6: The UK has a health-related ‘lost worker’ problem

The UK’s growth outlook looks brighter

The UK economy started the year strongly (see here) with upwardly-revised growth of 0.7% Q/Q. The signs from higher-frequency and forward-looking indicators are that momentum has moderated somewhat this quarter, but we still believe that the Q1 expansion will mark an inflection point after an extended period of stagnation for the UK economy. Consumer spending is set to be the main driver with inflation now back at target but nominal pay growth still above 5% Y/Y. We think that the BoE will reduce its focus on wages and services inflation, which are backward-looking, and proceed with rate cuts – perhaps as soon as August (see here). (Against this background we’re still unsure why Sunak called the election when he did rather than wait for economic conditions to improve and borrowing costs to fall).

All told, we are cautiously optimistic on the UK’s growth prospects. Our current forecast is for GDP growth of 1.6% next year, which is slightly above the consensus. To our minds, the UK’s emergence from almost a decade of political instability is set to be the single most supportive factor when it comes to growth. With the French election sharply raising political risk in the euro area, the UK economy could increasingly be viewed as a relative beacon of stability in Europe (after a long period when the opposite was true) and we expect that will be reflected in better business investment figures. Over the longer-term, Labour’s proposed planning reform and more active industrial policy could also be growth-friendly if actually implemented, as would any easing in trade barriers between the UK and the EU. But structural issues (such as the health-related drop in activity rates – see here) will be hard to reverse, monetary policy will remain restrictive even after some cuts and there is limited scope for meaningful fiscal support. For that reason it’s hard to make a case for UK growth to exceed potential rates in the absence of supportive external conditions (e.g. a synchronised global upswing).